What is B2B buy now pay later (BNPL) and why platforms need it now

Team Parafin

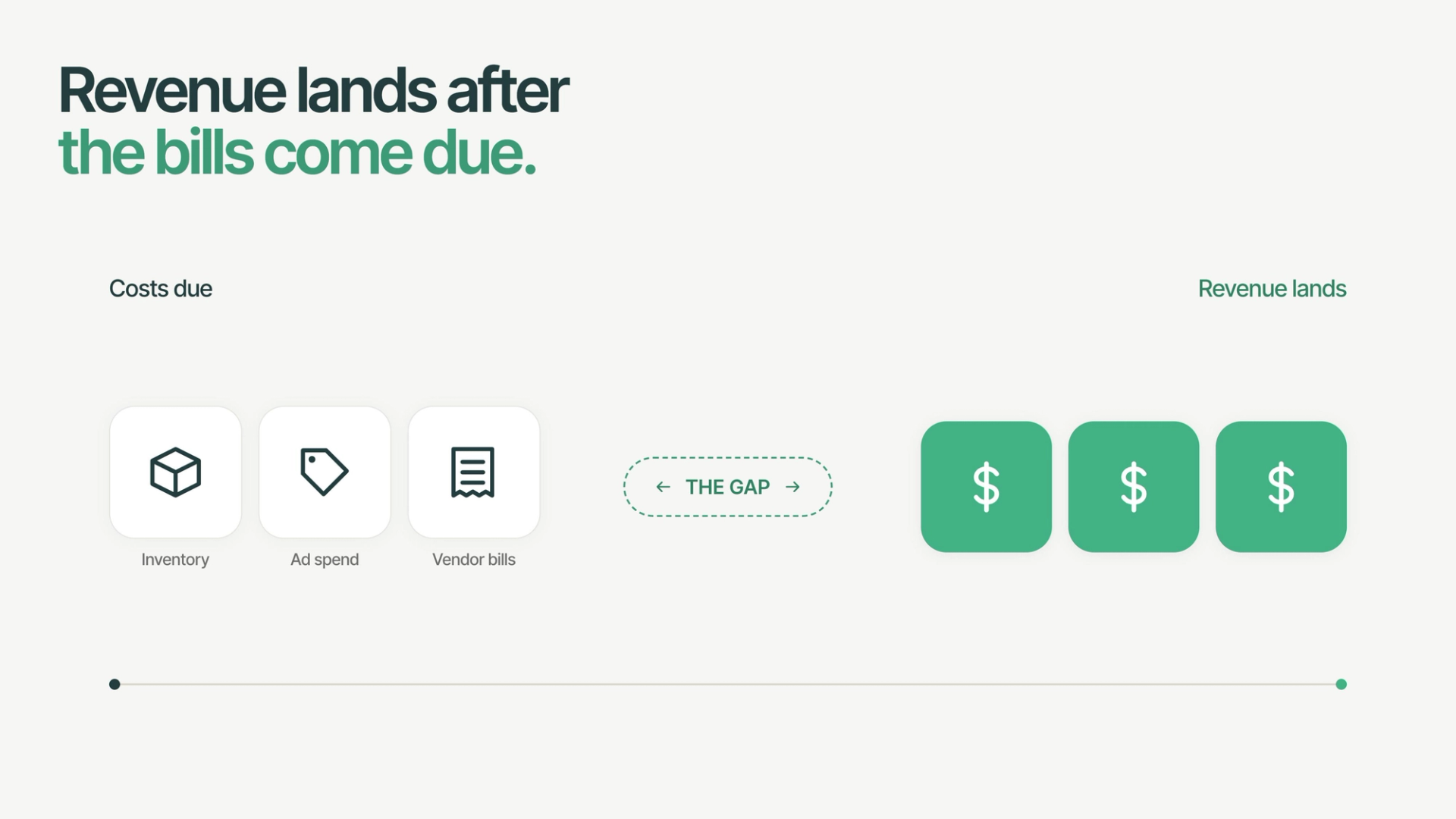

When a business buyer abandons a checkout because cash is tight, the B2B platform powering that transaction never sees it happen. There's no churn event, no support ticket, no exit survey. The order just doesn't happen. And the next one might happen somewhere else.

This is the problem inside platforms today. Small businesses live with a structural mismatch: inventory, payroll, and ad spend come due before revenue lands. 51% of small business owners say limited access to capital is restricting their ability to invest, expand, or operate at ideal capacity. Many lack business credit cards, or have reached their limits.

That constraint shows up first inside the platforms they already use. At checkout and on invoices, it looks like smaller orders, skipped purchases, and slower reorder cycles. The platform absorbs it as lower GMV and softer retention, often without realizing why. And it lands at a moment when platforms are already under pressure: as subscription fees compress, every point of GMV and every retained buyer matters more.

What B2B BNPL is and what it does for platforms

B2B buy now pay later (BNPL), often called pay over time, is designed to solve exactly this mismatch. It lets businesses purchase goods or services today and pay over time, with financing embedded directly into checkout, invoice, or other transaction flows. Approvals happen in seconds. Repayment is aligned to how businesses actually operate.

Unlike consumer BNPL, pay over time is built for business purchasing. Order sizes are larger, and underwriting is based on real business activity, not personal credit.

For platforms, the impact is structural and immediate. Embedding pay over time drives repeat usage, improves buyer retention, increases conversion, lifts average order value, and introduces a new revenue stream, without requiring the platform to take on credit risk.

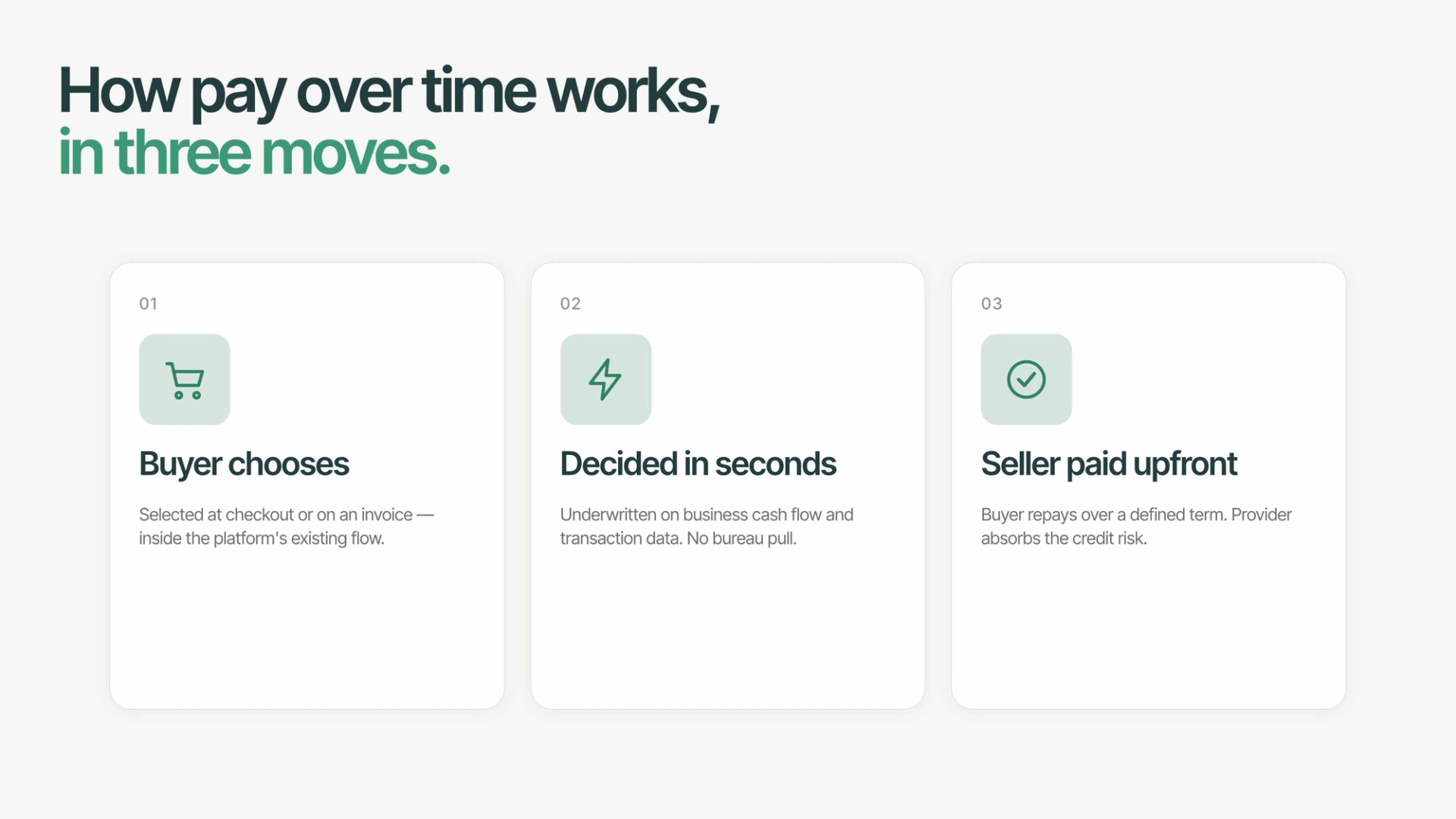

In practice, pay over time appears at the moment of transaction as an alternative to “pay in full.” A business buyer selects financing at checkout or on an invoice, gets a decision in seconds, and completes the purchase. The financing provider pays the seller upfront, and the buyer repays over a defined term, whether Net 30, Net 60, or installments over time.

How pay over time works

Behind the scenes, the platform integrates with a financing provider that underwrites, funds, services, and holds the receivable. The platform's role is to surface the financing option in the right place at the right time, and to earn a share of the resulting revenue.

What makes pay over time distinct is not just the repayment structure, but where and how it operates. Pay over time is embedded directly into the transaction flow and underwritten in real time using business cash flow and bank transaction data. There is no separate application, manual review, or reliance on personal credit.

Where pay over time shows up across B2B platforms

The mechanics shift slightly by use case, but the underlying need (bridging cash flow timing) is the same.

B2B commerce. For marketplaces and direct seller platforms, pay over time replaces the financing methods small businesses default to today. It competes with business credit cards, which carry personal guarantees and limits that don't scale, and with in-house net terms programs that put credit risk and collections on the seller's balance sheet.

Invoicing and vertical SaaS. AR automation, bill pay, and vertical SaaS platforms sit in the flow of B2B payments but often lack embedded financing. Pay over time fills that gap: the provider pays the supplier immediately, the buyer repays on flexible terms, and the platform earns a new revenue stream on top of existing fees.

Advertising spend. Ad spend is recurring, results lag the spend cycle, and buyers frequently hit credit card limits before they can scale campaigns. Pay over time lets buyers commit to larger campaigns and spread payments across the billing cycle, driving higher spend per advertiser and reducing checkout drop-off.

Payroll. For payroll platforms, pay over time fills a different cash-flow gap, funding payroll runs on deferred terms when revenue timing is off. See how Gusto launched embedded pay over time for a deeper look.

What changes when pay over time is embedded

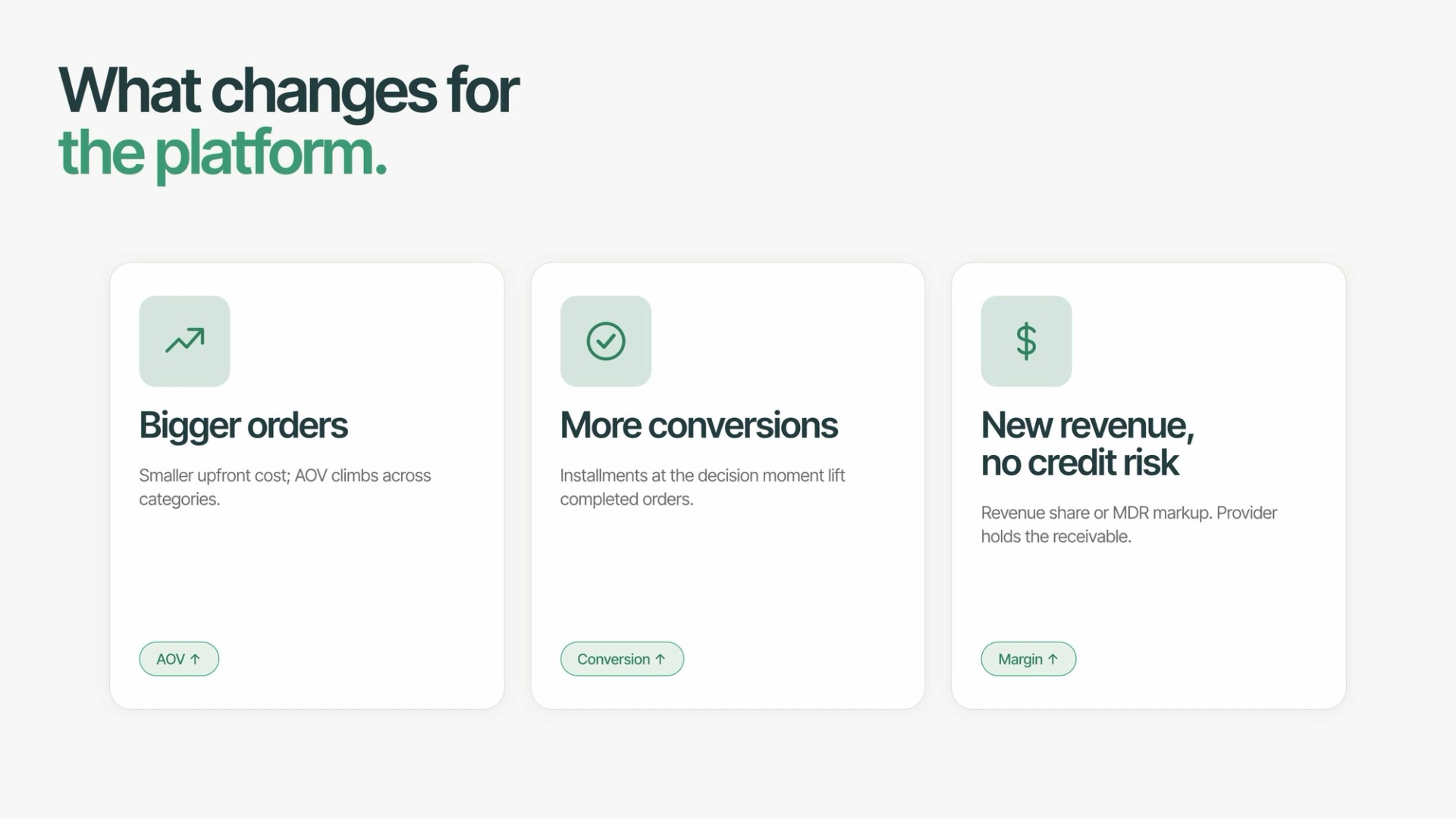

Business buyers with access to financing at the point of purchase tend to spend more per transaction. When cost is spread over time, larger purchases become easier to justify, increasing average order value.

Because pay over time is embedded directly into the checkout or invoice flow, it is selected at the moment of need, not applied for separately. This drives higher adoption compared to standalone financing products.

Access to financing turns one-time purchases into ongoing relationships. Buyers come back and reuse credit as part of their normal workflows, increasing retention and lifetime value.

Pay over time creates a direct revenue stream through revenue share or MDR markup, without requiring the platform to take on credit risk or manage servicing. Sellers get paid upfront, while the provider handles underwriting, collections, and risk.

Why now?

Two market shifts are accelerating adoption. First, the US market has dramatically fewer liquidity options than its international peers. Factoring represents roughly 12% of GDP, creating significantly higher demand for embedded credit at the point of payment in the US.

Second, deferred terms are already the standard expectation in B2B commerce. The behavioral shift pay over time asks of buyers is smaller than it was for consumer BNPL at retail checkout, so adoption curves trend faster, not slower.

What good pay over time looks like

Not every pay over time product works the same way. The two places where providers most clearly diverge are how they fit alongside other financing options, and how they underwrite.

Not consumer BNPL, trade credit, or a one-time loan

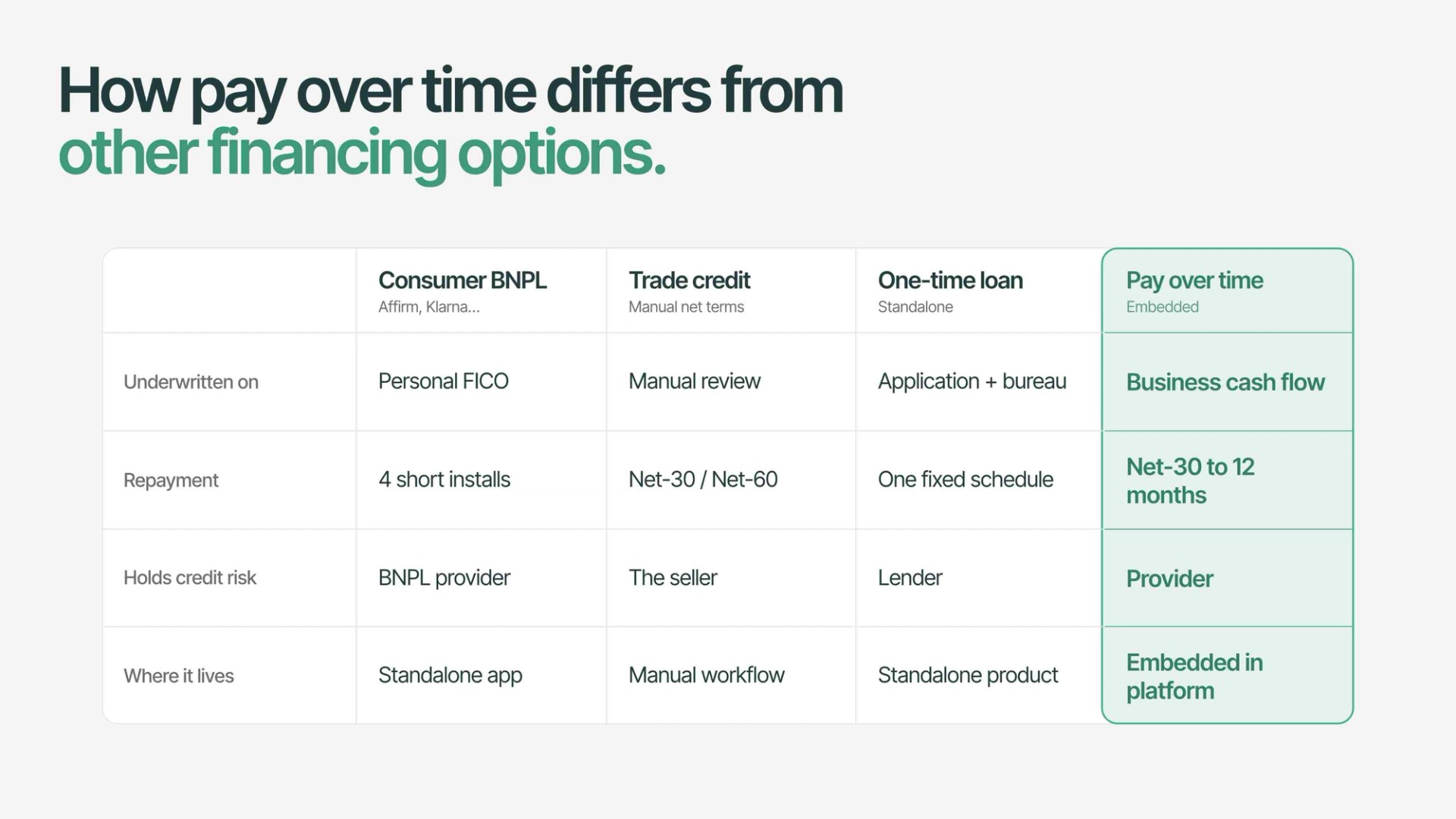

Not consumer BNPL. Consumer BNPL (Affirm, Klarna, etc.) scaled around a specific profile: small consumer purchases, short installment plans, and underwriting based on personal credit. B2B purchasing looks nothing like that. The differences show up in three places:

- Underwriting input: Consumer BNPL uses personal credit scores. Pay over time underwrites on business cash flow and transaction-level platform data, because most business buyers don't want their personal credit on the hook for a working capital purchase.

- Order size and repayment: Consumer BNPL is designed for relatively small, fixed purchase amounts with installment plans up to ~3 years. B2B transaction sizes vary widely, from advertising spend to large wholesale restocking, and require deferred terms, multi-month installments, or revolving lines.

- Credit reporting risk: As consumer BNPL data becomes incorporated into mainstream credit scoring models, missed payments may negatively impact a buyer’s personal credit profile. By contrast, business-focused pay over time products are often underwritten using business activity and cash flow data rather than consumer credit alone.

Not trade credit. Traditional trade credit is manually evaluated and extended from the seller's balance sheet, with the seller owning credit risk, collections, and bad debt. Platform-embedded pay over time transfers all of that to the financing provider: approvals happen in seconds using cash-flow-based underwriting, terms extend from Net 30 to 12-month installments, and even thin-file businesses can qualify.

Not a one-time loan. A loan is a discrete event: one application, one fixed amount, one repayment schedule, with funds deposited into the borrower's bank account as fungible cash. Pay over time is transactional and revolving. A buyer draws against a credit line at the point of purchase, within their existing platform workflow, and funds are disbursed directly to the service provider, not to the buyer. Each draw is tied to a specific transaction with its own repayment schedule, making the capital non-fungible by design.

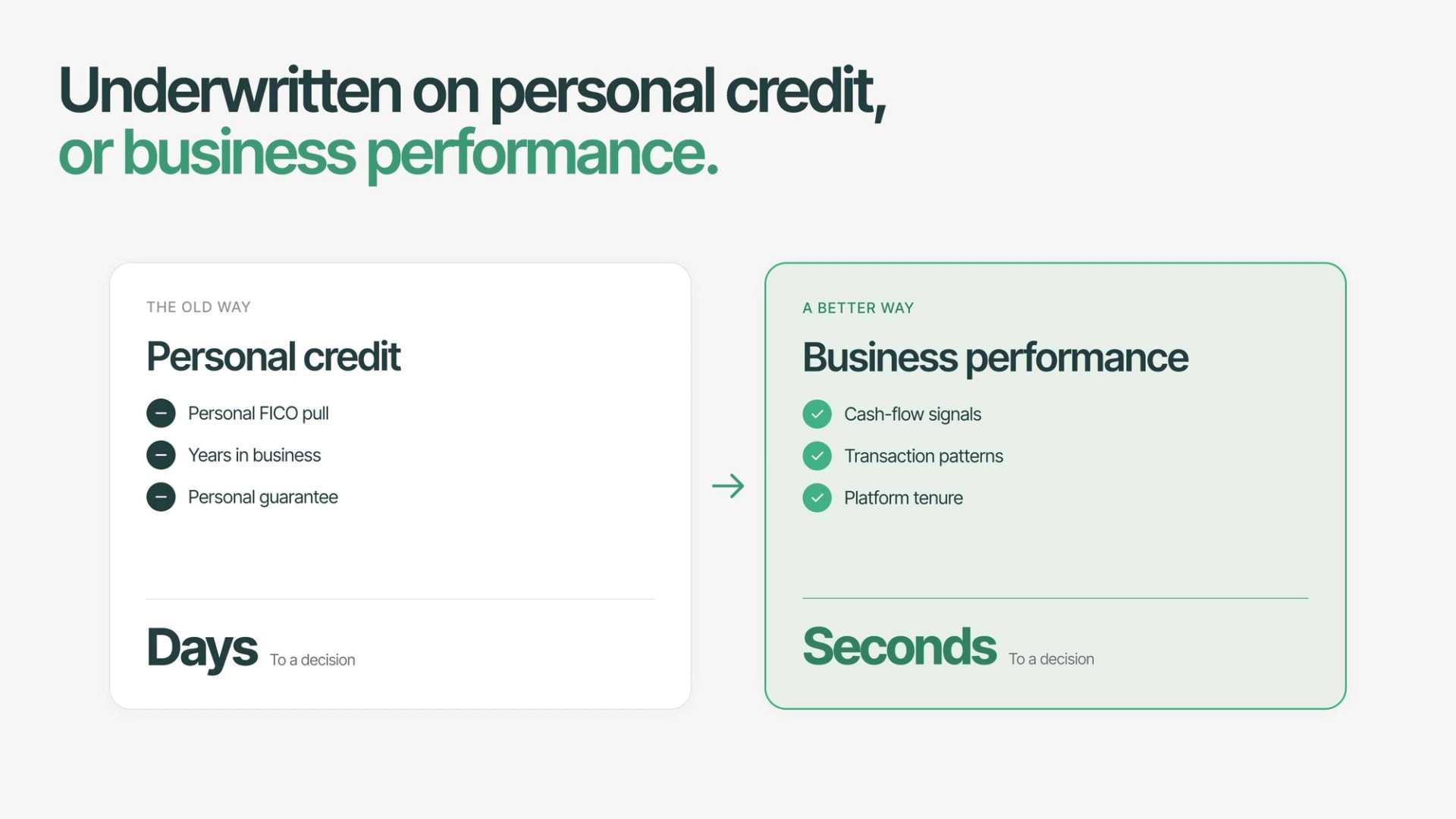

Underwriting built on business performance

Underwriting is where pay over time providers diverge most, and it shapes everything downstream: approval rates, buyer experience, and which small businesses can actually access the product.

Some providers still rely on credit bureau data or personal guarantees. That approach has three real costs. It co-mingles personal and business liability, putting the owner's credit on the hook for a business purchase. It carries documented biases against women, minority, and immigrant founders, even when their businesses are profitable. And it caps credit at what the individual can personally support, rather than what the business can actually service.

The strongest models underwrite against business performance instead: cash flow, transaction patterns, and platform tenure. The business is judged on its own merits, credit scales with revenue, and approvals don't depend on the owner's personal financial history.

What platforms miss by moving slow

Pay over time is no longer a question of whether platforms should offer financing at the moment of transaction. It’s a question of whether they move now or let a competitor get there first.

Leaders treat pay over time as infrastructure, building programs that scale with their ecosystem and support buyers through cash flow volatility. Laggards treat it as a feature, underestimating the complexity or relying on solutions that don’t adapt.

The cost of waiting is often invisible. When platforms can’t support buyers through cash flow constraints, those buyers don’t announce they’re leaving. They transact less, reorder elsewhere, or form new dependencies with whoever surfaces capital first. By the time it shows up in retention, the opportunity has already shifted to a competitor.

See how Parafin helps platforms launch and scale embedded pay over time. Talk to our team.