What is embedded capital and why platforms need it now

Team Parafin

Access to capital is the breaking point for many small businesses. When cash runs short, owners are not thinking about optimization or long-term growth. They are thinking about making payroll next Friday, restocking inventory before the weekend rush, or spending on last-minute advertising to avoid another slow weekend.

Capital does more than help businesses get through these moments. It also determines whether they can invest in growth, such as purchasing new equipment, expanding staff ahead of demand, or opening a second location when momentum is there.

For most SMBs, cash-flow volatility is a constant. Short-term gaps between revenue and expenses are common, and access to timely capital shapes how businesses respond. Without it, they are forced to react. With it, they can plan ahead and act on opportunities to grow.

What is embedded capital?

Embedded capital is financing built directly into the software platforms small businesses already use. Eligibility, pricing, and repayment are informed by platform-provided data and delivered inside existing workflows.

Rather than asking businesses to leave the tools they rely on and apply for a traditional loan, embedded capital meets them at the moment capital is needed, using signals the platform already has.

What embedded capital actually looks like

Traditionally, small businesses have accessed capital outside the platforms where they do their day-to-day work. Bank loans rely on lengthy applications, personal credit checks, manual reviews, and fixed repayment schedules built around the assumption of stable cash flow. Earlier generations of alternative online lenders may move faster, but often do so through high-cost, rigid products that shift risk back onto the business. In many cases, this locks SMBs into predatory cycles of debt. And in both models, access to capital is disconnected from how the business actually operates.

Embedded capital takes a fundamentally different approach.

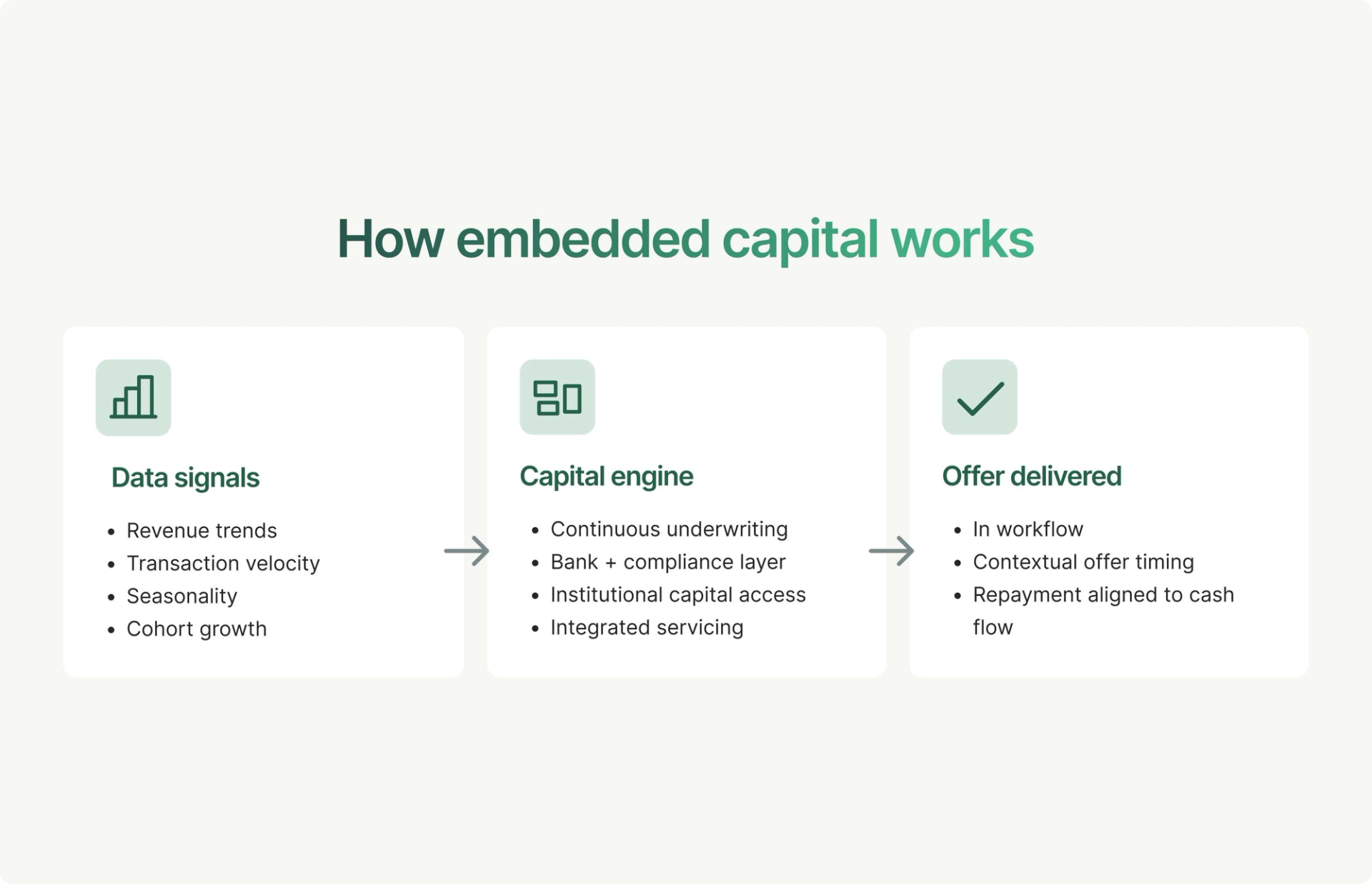

Financing is built directly into the platform itself, extending the tools businesses already use to run their operations. Eligibility, offer sizing, and timing are informed by platform-provided data, including revenue trends, transaction volume, seasonality, and growth patterns, rather than static applications or extensive financial statements and documentation.

In practice, capital is surfaced inside existing workflows, and in context, appearing at moments when businesses are already making operational decisions around scheduling, payments, and customers. On a vertical SaaS platform like Xplor, which supports fitness studios, field service companies, and other local service businesses, this means funding appears at the moment it is most useful. A landscaper preparing for the summer rush may see a pre-approved offer sized to cover new equipment or staffing. A fitness studio may access capital ahead of a growth season to add equipment or secure a second location. Either way, the business does not leave the platform, fill out new paperwork, or wait weeks for a decision.

Repayment can be designed to align with how a business generates cash, using structures that reflect operating reality, whether through automated deductions tied to daily sales payouts or more traditional schedules adapted to a merchant’s maturity and needs. This flexibility helps businesses manage slower periods without the strain of rigid repayment assumptions.

This model only works if underwriting is both fast and accurate. Rather than relying on narrow proxies like personal credit scores, underwriting draws on platform-provided performance signals and automated risk analysis. At scale, this requires continuous evaluation, not because platforms are responsible for managing risk, but because capital providers must regularly reassess performance as new data flows in and business conditions change.

Delivering capital this way requires more than simply offering a loan. Embedded capital depends on infrastructure that connects underwriting, capital markets, compliance, and servicing behind the scenes. From the merchant’s perspective, this complexity is invisible. From the platform’s perspective, it is what makes capital reliable, scalable, and safe to offer over time, without requiring the platform itself to become a lender.

When small businesses cannot access capital, platforms absorb the risk

Platforms sit at the center of how modern small businesses operate. They are where revenue flows, where work happens, and where trust already exists. That position creates opportunity, but it also creates exposure.

Many platforms already support the earnings side of the equation. They help businesses sell more, get paid faster, and operate more efficiently. But earnings alone do not solve small business cash flow problems. When cash gaps emerge, whether short-term or structural, the impact shows up inside the platform.

The pattern holds across platform types. For a restaurant owner selling through DoorDash, cash flow pressure may show up as payroll. Revenue fluctuates week to week, but wages do not. A traditional loan takes too long, and fixed repayments introduce risk the business cannot afford. In moments like these, access to capital is the difference between reacting and planning. Too often, small businesses are forced to react.

That reality is widespread, not exceptional. In the past year, 81% of small businesses that sought credit struggled to access affordable capital, and many did so simply to cover operating costs. Cash-flow volatility is not an anomaly. It is a structural feature of the small business economy. These are the baseline conditions under which most merchants on any platform operate.

This creates a structural risk for platforms. Even when a merchant’s underlying business is healthy, a temporary cash gap can push them into decline, or in some cases, insolvency. Without a way to intervene, platforms absorb that risk indirectly through lost volume, weaker retention, and stalled growth. Just as importantly, they leave growth on the table. When platforms can’t support merchants through moments of constraint, those businesses are forced to seek capital elsewhere, often forming new dependencies at the exact moment they should be deepening their relationship with the platform.

Embedded capital changes that dynamic. It gives platforms a way to support merchants at the moment capital matters most, inside workflows they already trust. That’s why embedded capital isn’t just another financial feature, but becoming a core platform capability.

Why capital programs can no longer be delayed

Several forces are converging at once, and together they make delay costly.

Interest rates remain elevated and traditional small business loans are slower and harder to access, especially for newer or non-traditional businesses. As a result, small businesses are turning to financing options that prioritize speed, relevance, and flexibility. When platforms do not offer a clear path to capital, merchants are forced to look elsewhere at the exact moment they need support.

At the same time, merchant expectations have shifted. According to Worldpay’s 2025 Merchant Insider Report, 1 in 5 businesses would leave their current platform for one with better payments and financial capabilities, and 90% now consider access to financial products critical to their operations. When a platform already has visibility into a merchant’s revenue, seasonality, and performance, it feels increasingly reasonable to expect that same platform to facilitate access to capital.

In this environment, every quarter without a capital program is not neutral. It compounds competitive disadvantage and represents a missed opportunity to retain and grow the businesses that already trust the platform.

Without capital, merchants may not survive, and they churn

When small businesses can’t access capital, some of them don’t make it. When they fail, they leave the platform entirely. Churn driven by financial constraint is especially painful because it’s often preventable. The merchant didn’t leave because the product failed them. They left because they ran out of options.

Long before failure, the strain is already visible. According to a 2025 report from the Small Business & Entrepreneurship Council, 51% of small business owners say limited access to capital is restricting their ability to invest, expand, compete, or operate at full capacity. That constraint shows up as hesitation, pullback, and disengagement, all of which platforms feel before a merchant ever churns.

As one Parafin-supported merchant put it, “Having payments automatically calculated based on our sales removed the pressure of traditional financing. We used the capital to build inventory, and the flexible terms aligned perfectly with our business operations.” In moments like these, capital shifts from a reactive to proactive, supporting merchant stability and long-term growth.

Capital drives measurable platform growth

The case for embedded capital isn’t just emotional; it’s measurable. When designed well, capital programs drive growth across the metrics platforms care about most.

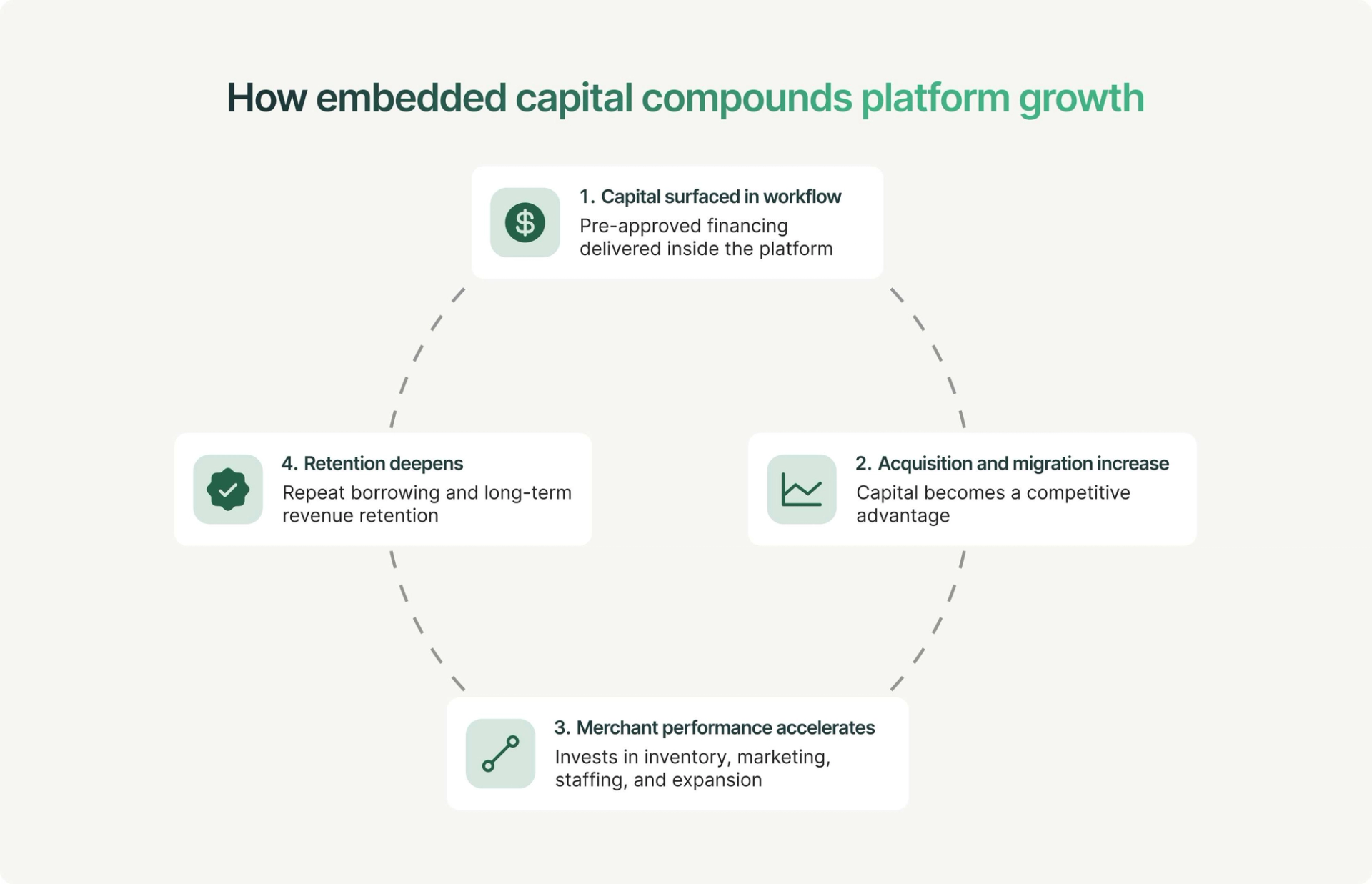

Capital increases gross merchandise volume (GMV)

Across large commerce, payments, and vertical SaaS platforms, merchants who receive embedded capital consistently grow faster than peers without access to funding. By enabling businesses to invest in inventory, marketing, staffing, and expansion, capital unlocks growth that compounds back into the platform through higher transaction volume and stronger merchant performance.

Capital drives retention

Access to capital changes how merchants relate to a platform. It increases reliance, trust, and long-term engagement. Across Parafin-powered programs, 85% of first-time borrowers go on to take a second advance, and Parafin programs see greater than 100% cohorted revenue retention.¹ Capital becomes part of how merchants run their businesses, not a one-time interaction.

Capital fuels acquisition

Embedded capital also influences how merchants evaluate and adopt platforms. In one Parafin-powered case study, platforms saw a 48% increase in merchants migrating after introducing capital. More broadly, 87% of merchants say they’re more likely to try a new product when it’s offered directly by a platform they already trust, making capital a meaningful acquisition and differentiation lever.¹

Why embedded capital is harder than it looks

The promise of embedded capital is compelling. But moving from early traction to a durable, scalable capital program requires more than a clean interface. The real work lives in the infrastructure needed to operate capital safely, reliably, and over time.

Launching a capital program involves a set of tightly connected capabilities: underwriting, capital markets access, sponsor bank and regulatory compliance, payments, fraud and risk management, and ongoing program operations. Each layer introduces complexity and real risk, and that complexity increases as programs scale.

That complexity is often underestimated because early progress can look deceptively simple. At scale, underwriting is not a one-time decision, but an ongoing evaluation exercise. As new platform-provided data flows in and merchant behavior changes, risk and performance expectations must be continuously reassessed by the capital provider. This isn’t a burden platforms should carry themselves, but it is essential to operating a capital program that remains healthy through cycles.

While a platform may be able to raise debt, secure a bank sponsor, and build a user interface, long-term program success depends on managing all the moving pieces in lockstep. Capital structure, underwriting, compliance, servicing, product design, and user experience must work together seamlessly. General working capital, credit cards, and point-of-transaction financing all depend on the ability to operate this system cohesively over time, not just at origination.

Even with strong infrastructure in place, embedded capital is not one-size-fits-all. Program design varies based on merchant profile, geography, regulatory exposure, and platform economics. Risk tolerance differs. Repayment mechanics differ. Compliance requirements differ. What works for one platform may not work for another.

The most effective embedded capital programs are built with flexibility at their core. They evolve as merchant needs change and as performance data accumulates over time. Platforms that partner with experienced capital providers gain the ability to adapt safely, without locking themselves into rigid structures that turn capital from a strategic advantage into an operational constraint.

What best-in-class embedded capital looks like

Best-in-class embedded capital programs turn complexity into leverage.

Rather than forcing platforms to become lenders overnight, they rely on infrastructure that handles the full lifecycle of capital: underwriting, bank partners, funding, compliance, servicing, and support behind the scenes. That separation allows platforms to extend capital confidently without taking on operational or regulatory burden that would distract from their core product.

This is where trust compounds. Businesses trust platforms because they already sit at the center of how work gets done. Platforms can only extend that trust if the capital experience is consistent, transparent, and reliable at scale.

When done well, end-to-end programs unlock structural advantages:

- Faster time to market and pure profit from day one, with compliance, risk, and servicing infrastructure already in place

- Pricing that reflects reality, driven by real operating data rather than static assumptions

- Durable access to low-cost capital, enabled by the scale and long-term capital markets relationships behind end-to-end programs

- Room to evolve and experiment, as structures and eligibility adapt over time without rebuilding from scratch

Over time, these advantages compound. Capital stops being a one-off product decision and becomes part of the platform’s operating fabric.

What separates leaders from laggards

Embedded capital is no longer a question of whether platforms should offer financing. It is a question of how seriously they are willing to invest in doing it well.

Leaders treat capital as infrastructure. They design programs that scale with their ecosystem, support merchants through volatility, and evolve as business conditions change. Laggards treat capital as a feature. They underestimate the complexity, delay commitment, or rely on brittle solutions that struggle to adapt.

The gap between the two widens over time.

Platforms that meet small businesses at their fundamental point of need, providing access to capital when it matters, build relationships rooted not just in transactions, but in long-term support. When small businesses grow, platforms grow with them.

See how Parafin helps platforms launch and scale embedded capital, without taking on the complexity behind the scenes. Get in touch here.

¹ Source: Parafin internal analysis of anonymized merchant performance data across Parafin-powered programs, 2025.