Why SMB cash flow volatility is a platform problem

Team Parafin

A merchant can be profitable every month of the year and still be the reason your transaction volume drops in Q3.

Anita Gibbs, COO of 360 Payments, put it plainly: "It's a cyclical market. Sometimes our customers just need a little help to make payroll during slow seasons or buy parts for a really big engine rebuild so they can finish the job."

She was talking about independent auto shops: owner-operators who are good at their work, have the customers, and win the jobs. What they don't always have is the cash on hand to start them. And when they can't start the job, 360 Payments doesn't process the payment.

This is the practical consequence of small business cash flow volatility, and it plays out on platforms every day.

SMB cash flow is often framed as a management problem. In reality, it’s structural. And when merchants experience liquidity gaps, the impact doesn't stay on their balance sheet. It shows up directly in the metrics of the platforms they run their business on.

The connection between merchant liquidity and platform economics is direct. Across more than 2 million merchants on Parafin's platform, nearly 6 in 10 experience at least one week with zero recorded revenue.¹ Those aren't businesses in distress. They're operating normally, with seasonal slowdowns, brief closures, gaps between projects. But each zero-revenue week is a moment when cash reserves draw down and margin for error shrinks.

When that margin disappears, merchants pull back. And platforms feel it.

Why small businesses run out of cash (and why traditional lenders miss it)

Profit is an accounting measure. Cash flow is what's in the bank.

The two diverge whenever there's a timing gap between when money goes out and when it comes in. For small businesses, those gaps are everywhere:

- A contractor buys materials in March. The project completes and the invoice gets paid in May.

- A retailer places a wholesale order in August for fall inventory. Revenue arrives in October.

- A restaurant pays food suppliers Monday for a weekend rush that won't settle until Friday.

- A service business runs a customer acquisition campaign in January. The new regulars it generates become revenue over the following quarter.

In each case, the business is solvent on paper. It may not have enough cash to cover payroll on any given Tuesday.

According to the Federal Reserve’s 2025 Small Business Credit Survey, 51% of small firms report uneven cash flow as a financial challenge, making it one of the most common issues facing small businesses. A separate 2025 Bluevine survey found that nearly 4 in 10 small businesses have less than one month of operating expenses in cash reserves.

This is the baseline condition for a significant share of small businesses.

Why traditional lenders struggle to see SMB cash flow volatility

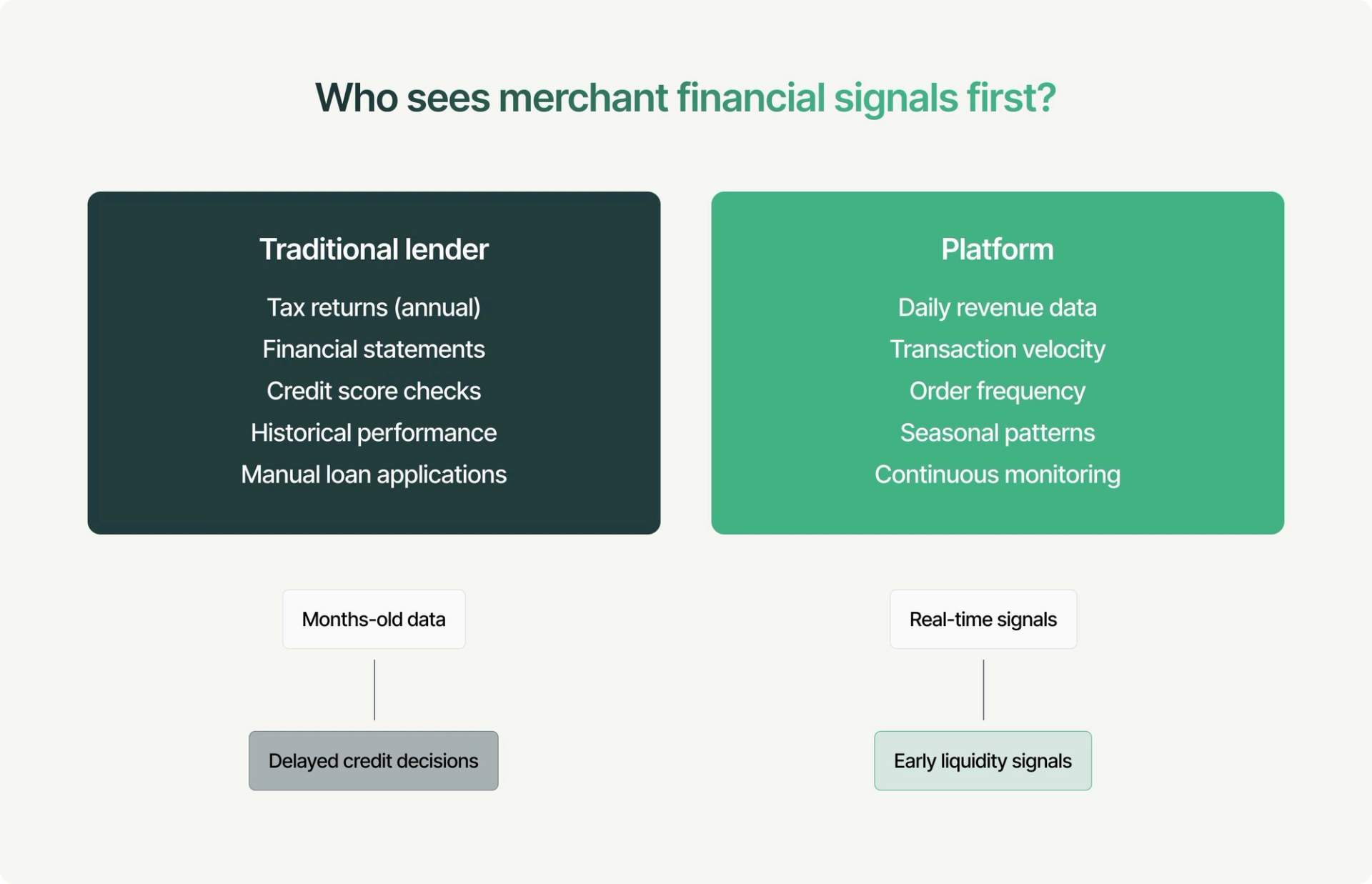

The liquidity gaps that matter most to merchants are often invisible to traditional financial institutions. Banks assess creditworthiness using backward-looking data: tax returns, annual statements, credit scores. These tools work reasonably well for evaluating stable, asset-heavy businesses. They're not always well calibrated for the operating rhythms of high-volume, lower-margin SMBs, where a cash flow gap can open and close within a single week. By the time a seasonal shortfall shows up in annual financials, it's already resolved or it's already done damage.

The result is a structural mismatch. Small businesses with genuine liquidity needs, operating in predictable and observable patterns, regularly fail to qualify for credit products designed around a different type of borrower. Only about 41% of small businesses that apply for financing receive the full amount they seek, leaving many entrepreneurs to turn to alternative sources of capital.

Platforms, on the other hand, operate from a fundamentally different vantage point. They see merchant activity like sales volume, order frequency, payout patterns, and reversals, at a daily or even hourly granularity. No quarterly financial statement can replicate this.

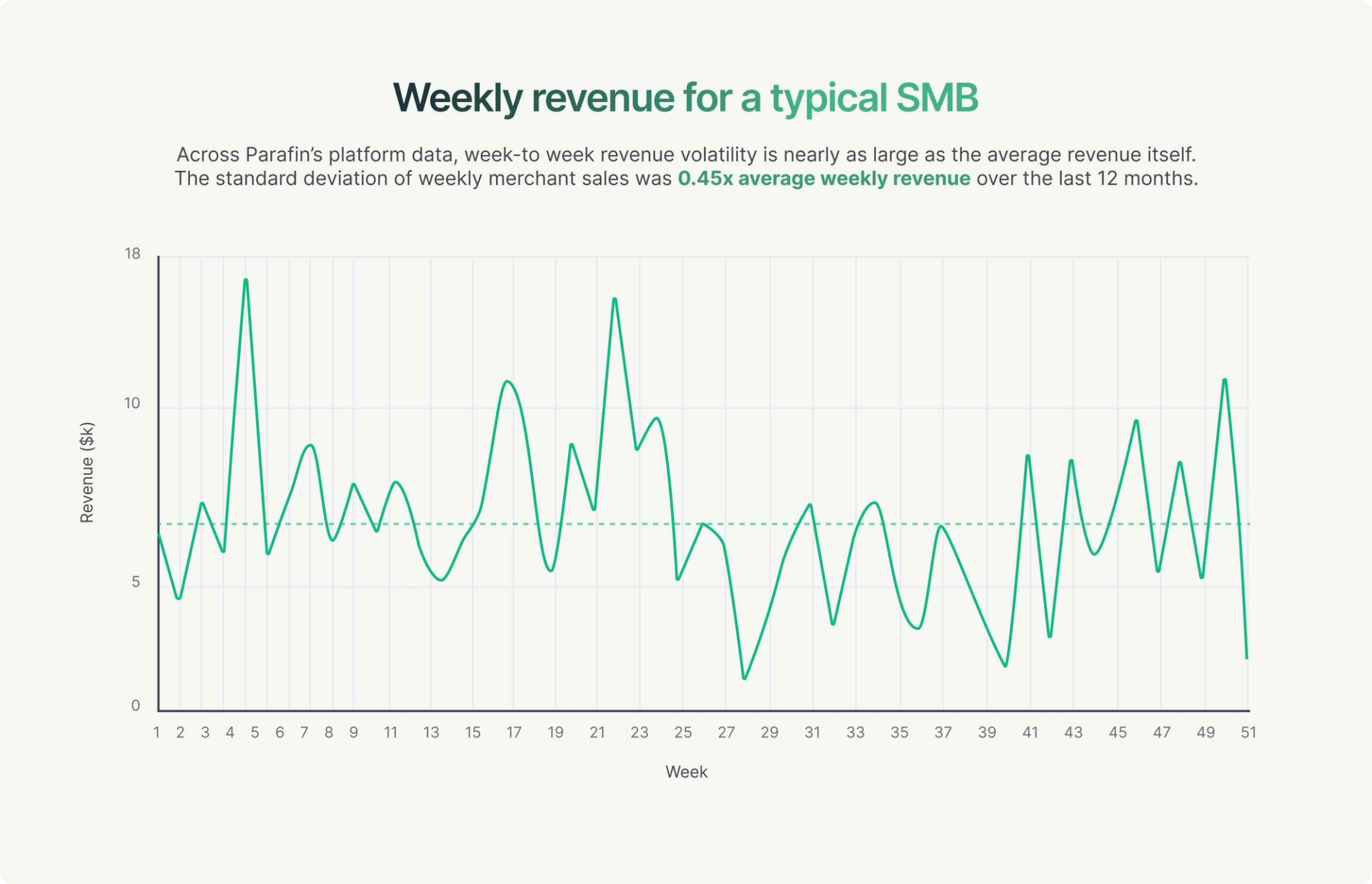

Parafin's platform data shows that week-to-week revenue swings for a typical merchant are nearly as large as the average revenue itself. The standard deviation of weekly sales across the merchant population was 0.45x average weekly revenue over the last 12 months.² Revenue doesn't move in a steady line. It spikes and drops constantly.

Platforms observe those movements as they happen. Traditional lenders find out months later, if at all, and that informational advantage matters. A platform that can see a merchant's liquidity pressure forming, before the merchant applies for financing elsewhere and before the pullback shows up in GMV, is in a position to act on it. But most platforms still don’t act on what they can see.

How platforms can solve small business cash flow gaps with embedded capital

Most platforms today observe merchant cash flow stress and have no mechanism to address it. The problem stays with the merchant. The consequences land on the platform.

According to the National Federation of Independent Business, 54% of small business owners made capital investments in the last six months, from purchasing equipment to expanding facilities. Those investments often happen well before the revenue they generate arrives. When liquidity gaps emerge, they don’t just affect a single business. They shape activity patterns across every platform that business operates on.

Embedded capital changes this dynamic.

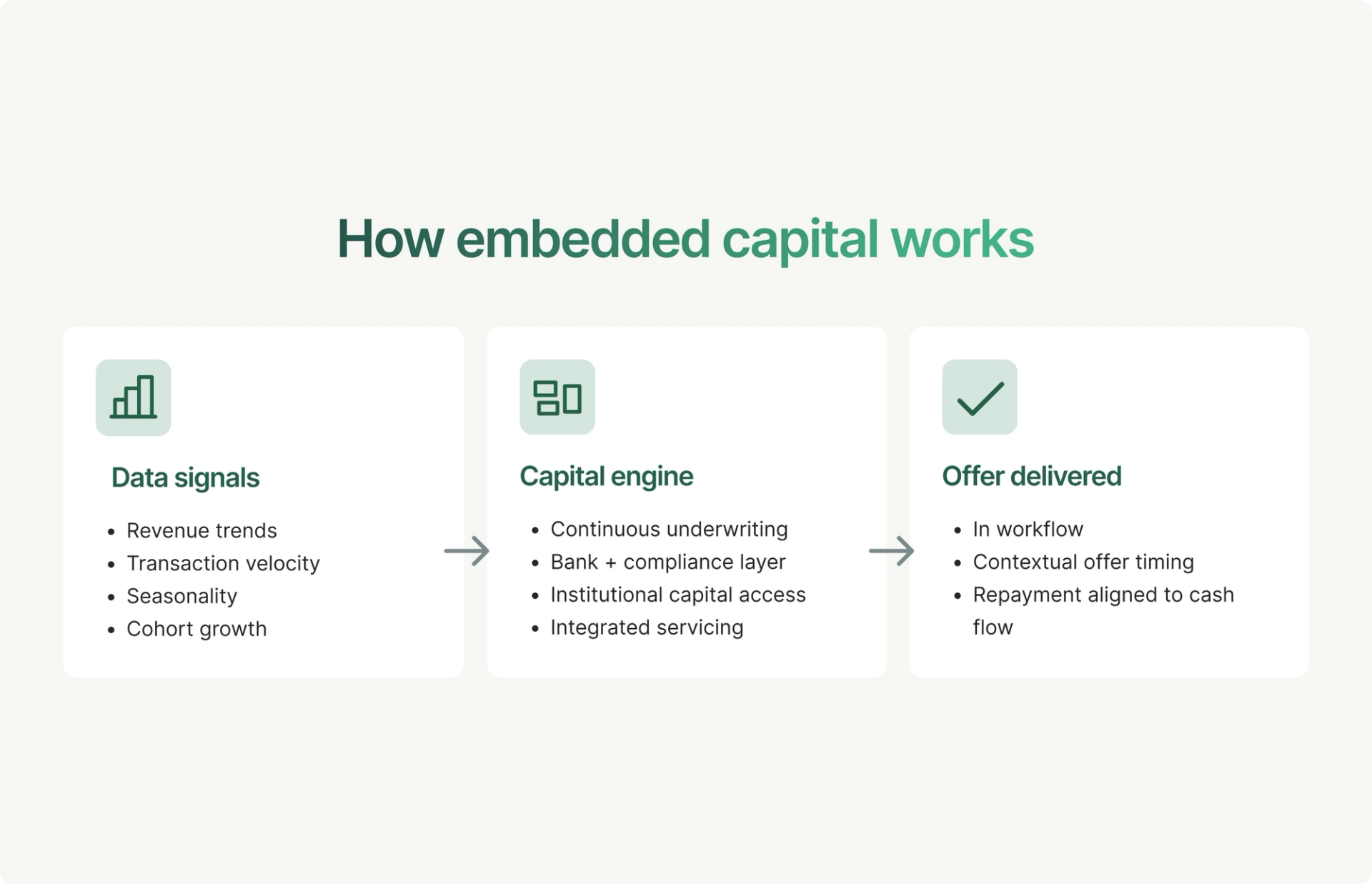

Platforms already see the signals that predict liquidity pressure: sales volatility, payout timing, order volume, and seasonal demand patterns. When financial infrastructure is built directly into the platform experience, that data can be used to deliver capital closer to when merchants need it.

Instead of applying for financing weeks later through a separate institution, merchants receive pre-approved offers calibrated to their actual revenue performance. Repayment adjusts automatically with sales rather than requiring fixed monthly obligations.

The result is a different financial model. Capital is delivered at the moment of need, underwritten using real operating data, and repaid in line with business performance.

For merchants, that means fewer moments where a temporary cash gap turns into a missed growth opportunity. For platforms, it means something just as important: merchant activity continues.

Small business cash flow volatility isn’t going away. The timing mismatches between expenses and revenue are structural features of how these businesses operate, not problems that better financial education will solve.

Platforms are already sitting on the data that makes it possible to address these gaps in a way traditional lenders never could. The question is whether that position gets used.

More broadly, financial services are increasingly moving into the platforms where businesses already operate. According to a recent analysis highlighted by the World Economic Forum, the embedded finance market could reach $7.2 trillion globally by 2030, reflecting the growing shift of financial products into digital platforms.

Platforms that move first aren’t just adding a product. They’re reinforcing the economic engine that drives their marketplace.

At Parafin, we work with platforms to embed capital directly into the tools small businesses already use to operate and grow. If you’re exploring how financial infrastructure could strengthen your platform’s merchant ecosystem, learn more about our approach to embedded capital.

¹ Based on Parafin platform data from April 2025–March 2026, across 2 million merchants with at least eight weeks of recorded sales activity during the period. A "zero-revenue week" is defined as any calendar week with no recorded sales on the platform.

² Based on Parafin platform data from April 2025–March 2026, analyzing weekly revenue for 2.2 million merchants with at least four weeks of recorded sales activity. Coefficient of variation calculated as the standard deviation of weekly revenue divided by average weekly revenue, measured at the individual merchant level and aggregated at the median across the merchant population.